From service to product: why most pivots fail

From service to product: why most pivots fail

From service to product: why most pivots fail

Every founder event I go to, someone asks me the same question. They run a service business, things are going well, and they have built a small internal tool, or a methodology, or a productised offer on the side. They want to know whether to flip the whole company into a product business.

I have been thinking about this question for seven years. My master thesis at Solvay was about exactly this: when, and how, a Belgian scale up should transform a professional service firm into a SaaS business. It won the de Barcy prize in 2019. Since then, as COO at dups, I have sat with dozens of Belgian founders weighing the same call. It is a fair question, and the honest answer has more nuance than people expect.

What I keep seeing is that most service to product pivots do not deliver what the founders hoped for. Not because they lacked talent, not because the market was wrong, but because the two business models are not adjacent. They are foreign countries. The pivot often gets framed as a strategy choice when it is closer to a company replacement.

Why the pivot is so seductive

The math is brutally in favour of product. A service firm trades at 1 to 2x revenue. A solid SaaS business trades at 5 to 10x ARR, sometimes more. Margins move from 10 to 15% to 40% and beyond. Growth stops being capped by headcount. You can sell in Brussels, São Paulo and Singapore from the same desk.

In 2014, when the Belgian data analytics firm I studied for my thesis faced this decision, the temptation was already enormous. SaaS was the gold rush. The investor narrative was unbeatable. They went for it. The founder said years later that he would not do it again. He would have spun the product out as a separate company and let the service business run on the side.

Today, with Lovable, Claude Code, v0, Cursor and the like, the seduction is even stronger. Any consulting firm can ship a working web app over a weekend. Any agency can wrap a recurring workflow into a SaaS in a sprint. The barrier to building a product has collapsed. The barrier to running a product company has not.

That is the trap.

The three things that usually get underestimated

When a service founder walks me through their plan to go product, I always come back to three things. They are not in the pitch deck. They are not in the business plan. They are what tends to break the pivot.

Leadership style

In a service business, you sell yourself. The founder is the product. You go on stage, you meet the client, you adapt the proposal, you flex on scope. Your team is versatile by design. Everyone is a generalist with a senior, a junior and a project lead version of themselves. You can pivot a delivery in a week if the client changes their mind.

In a product company, none of that is an advantage. You sell a piece of software to a clearly defined persona, with a clearly defined problem, at a clearly defined price. You measure activation, retention, churn, MRR growth. You manage a team of specialists: developers, product managers, designers, growth marketers, customer success. The founder who was brilliant at adapting to every client is now expected to say no to 90% of feature requests so the roadmap stays focused. That is a different person.

Some founders make that switch. Many do not, and not because they could not learn. The muscle they have spent ten years building is the wrong muscle for the new job, and rebuilding it in real time, with payroll to meet, is brutal.

Organisation

A service org is a pyramid. Versatile profiles, ranked by seniority. Margins come from utilisation rate. A product org is horizontal. Specialist functions, ranked by domain. Margins come from gross retention and scale.

Running both seriously under one roof is very hard. Many have tried. McKinsey Solutions tried. Most service firms that also have a product end up with a product line that is 5% of revenue and a large share of the management headaches. The two businesses fight for attention, for talent, for capital allocation. Investors tend to dislike it. They want one bet, not two.

If you go product, you have to be ready to part with a meaningful share of your consultants, hire 20 to 30 specialist profiles, and accept that the org chart you spent years building does not survive the transition.

Cash and time

A service business throws off cash from day one. Bill the client, collect, repeat. A product business runs the other way: you spend now, you collect later, often over years. AI tools have compressed the build phase, which I will come to in a moment, but the underlying cash dynamics still flip.

If you pivot, you typically stop being a self financed business and become a venture backed one. Different investors, different cap table, different reporting cadence, different exit pressure. You go from owning 100% of a profitable firm to owning 40% of a cash hungry one. That trade can absolutely be the right one. It is also not what most founders have in mind when they first say the word pivot.

What AI changes, and what it does not

AI has changed the cost of building. It has not changed the cost of running a product company, and in one specific way it has made the economics worse.

The case I studied in 2014 modelled product revenue taking 18 months to show up and three years to overtake the service. Today, with Claude Code, Lovable, v0, Cursor and the rest, you can ship a working v1 in weeks rather than months. The R&D bill is a fraction of what it used to be. What has not got easier is everything that comes after: distribution, customer success, support, sales hiring, retention, surviving the gap between an MVP and a product people will pay for year after year. The burn has shifted from R&D into go to market, and that line is still measured in years, not weeks. Especially in B2B, where sales cycles do not care how fast you shipped.

The harder problem is on unit economics. A lot of what gets pitched as a SaaS today is in reality a thin wrapper around an OpenAI or Anthropic API. The classic SaaS playbook (sell once, serve at near zero marginal cost, harvest 80%+ gross margins) does not hold when every active user costs you tokens. Many of these companies are running on subsidised compute, thin or negative gross margins, or both, and their pricing only works as long as model providers keep prices where they are. Not every AI product is in this bucket. Companies building proprietary data, deep workflow integration, or models fine tuned on assets they own can get to real defensibility. But the SaaS multiple is not automatic anymore. If you pivot expecting 5 to 10x ARR, you have to be honest about whether the business you are building actually looks like SaaS, or like a software priced service with a cloud bill attached.

The bar to standing out as a product company in 2026 is higher than it was in 2014. The bar to building one has collapsed. Both things are true at once, and most of the conversation focuses on the second.

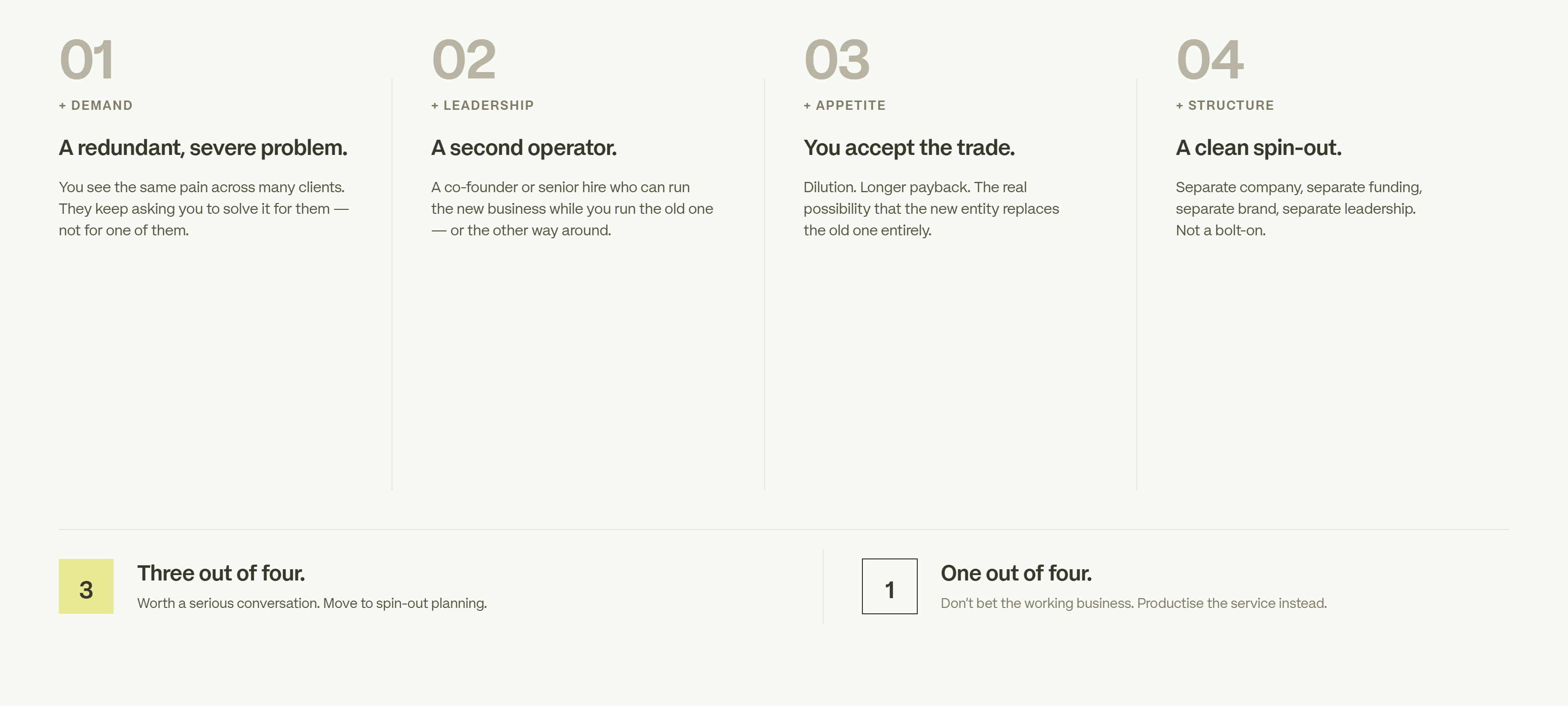

When the pivot does make sense

I do not tell every service founder to stay put. The pivot is the right call when four conditions are roughly in place:

- The product you would build solves a redundant, severe problem you have seen across many clients, and they keep asking for it.

- You have a cofounder or a senior hire who can run the product business while you keep the service running, or the other way around.

- You accept the dilution, the longer payback, and the real possibility that the new entity replaces the old one entirely.

- You can spin the product out as a separate company, ideally with separate funding, separate brand and separate leadership.

If three out of four hold, the conversation is worth having seriously. If only one does, the trade starts looking like a lottery ticket paid for with a working business, and that is a hard one to recommend.

The honest version

When I dig into the why with founders, the reasons that come up are real. Service businesses get tiring to scale. The valuation gap between service and product is genuine. Watching peers ship AI products with Lovable over a weekend creates real FOMO. I take all of that seriously, and I have felt versions of it myself.

But those reasons, on their own, are usually not enough to bet a profitable business on a model neither you nor your team has run before.

The more useful question, in most cases, is what would unlock the next phase of growth in the business you actually have. Sometimes that is productising a specific service into a fixed price offer. Sometimes it is verticalising into one niche where you become the default. Sometimes it is selling the firm to a strategic acquirer and using the proceeds to start fresh on the product side, with cash on the table and no dependency on the new entity working.

The pivot to SaaS is one option among several. It is rarely the only one, and not always the best one.

If you are thinking about it, I would be glad to have the conversation before the business plan is written rather than after.

Let's build your next deal together

Your sparring partner for fundraising, acquisitions, and exits. We bring legal and financial firepower, entrepreneur's speed, and direct access to the right capital.