European VC Q3 2025: the market keeps fragmenting

European VC Q3 2025: the market keeps fragmenting

European VC Q3 2025: the market keeps fragmenting

European venture dealmaking in 2025 is a story of extremes. While average deal sizes are climbing, overall activity is cooling, and capital is clustering around a handful of outsized AI rounds. The sector now commands nearly 40% of deal value YTD, with blockbuster raises from players like Mistral AI and Nscale setting the pace. But beneath the surface, follow-on funding is thinning, venture debt is slowing and exits hinge on a few headline IPOs. Klarna’s listing may have lifted spirits, yet the broader market remains fragile. What Q2 already made clear is now confirmed: European venture is compressing, not collapsing. Capital is still in play, but it’s flowing differently: fewer deals, larger cheques, and sharper scrutiny. The ecosystem is being reshaped: more fragmented, more cautious, and more reliant than ever on the AI boom.

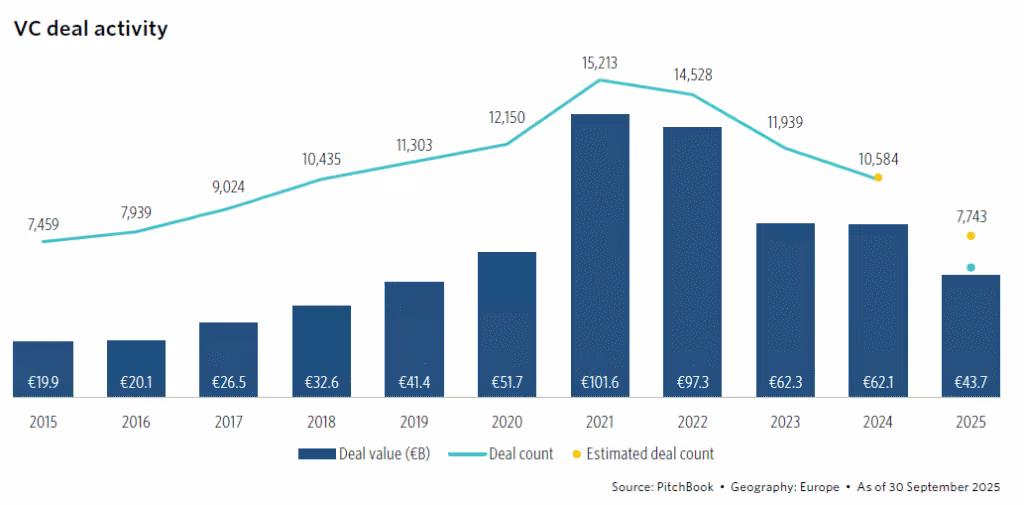

1. Deal activity shifts to a game of size over volume

The average ticket size is rising, with more rounds exceeding €25 million, especially in late-stage VC where activity held steady with just a 0,9% dip year-on-year. Venture growth, however, is trailing behind, down 13,6% compared to 2024. Unsurprisingly, AI remains the magnet for capital, with the top three deals: Mistral AI, Nscale, and Rapyd Financial Network raising over 3 billions combined. This concentration reflects a market increasingly shaped by fewer, larger bets, and a growing reliance on AI to drive a slowing momentum.

Regions know different resiliencies. Israel and Southern Europe continue to build on their Q2 acceleration, driven by a handful of standout deals. In contrast, the UK and Ireland are losing steam compared to last year.

2. AI’s dominance in European venture continues to deepen

Since Q1, its share of deal value has climbed steadily, reaching 39,1% of all VC deal activity in Q3. While impressive, this still trails the US, where AI accounts for nearly 60% of deal value. This sustained leadership is unusual and signals a structural shift in global tech markets. Yet, the AI label covers a wide spectrum: from startups built entirely on proprietary AI software to legacy platforms adding AI features, and even large retailers like Tesco and Walmart using AI to optimize operations. This diversity complicates thematic investing but also opens the door to differentiated exposure. This large AI vertical is now crowding out previously resilient sectors like life sciences and fintech, both of which saw deal values drop over 13% year-to-date.

Investor behaviour is also evolving. Geopolitical uncertainty has triggered a “flight to quality” since Q1, with due diligence cycles stretching beyond six months. Risk assessments, market conditions, and performance metrics are under closer scrutiny. Smaller, emerging managers are doubling down on sectors and geographies they know best, favouring precision over breadth.

Founders are adapting fast to the current macroeconomic uncertainty: hiring has slowed, burn rates are being trimmed, and AI-powered productivity tools are being deployed to stretch teams further. The result is a leaner, more focused operating model, one that reflects both caution and creativity.

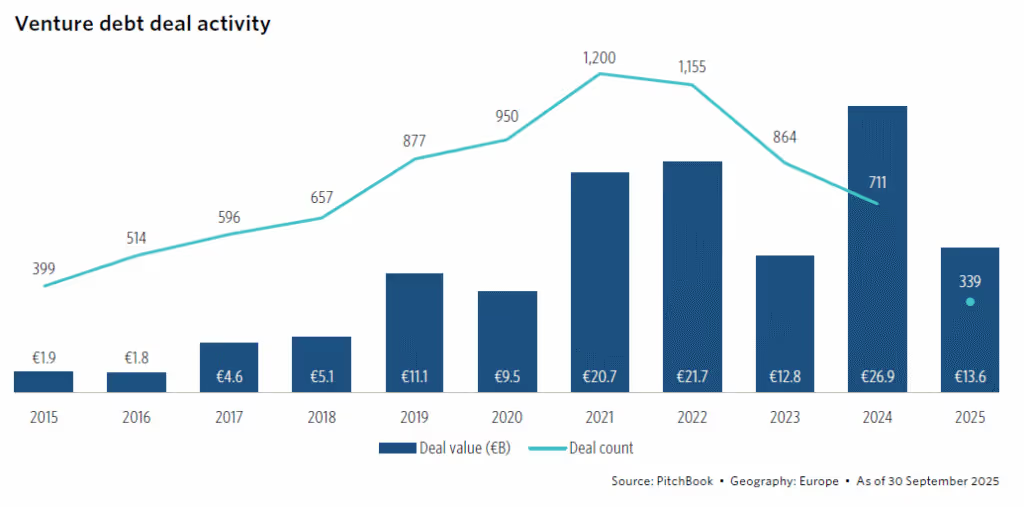

3. Venture debt in Europe is cooling after a strong start to 2025

Year-to-date deal value sits at €13,6 billion, pointing to a 32,6% drop compared to last year’s record. Fewer deals are closing, but the average size is rising, with 23% of Q3 rounds exceeding €25 million. Venture-growth companies now represent nearly 42% of all venture debt activity, up from 29% in 2024, showing a clear shift toward later-stage financing.

As IPO markets reopen, some companies are delaying debt raises in favour of public listings. Meanwhile, rate cuts across Europe are expected to support refinancing, with the ECB and Bank of England moving faster than the US Fed. Despite the slowdown, large deals continue to land: Jobandtalent raised €556 million, Electra secured €433 million, and Oura brought in €214 million. Fintech remains dominant, with British players like Ferovinum, Carmoola, and Wagestream each raising over €350 million in Q2. The year’s largest round came from Belgian company United Petfood in Q1, with a €1,4 billion raise.

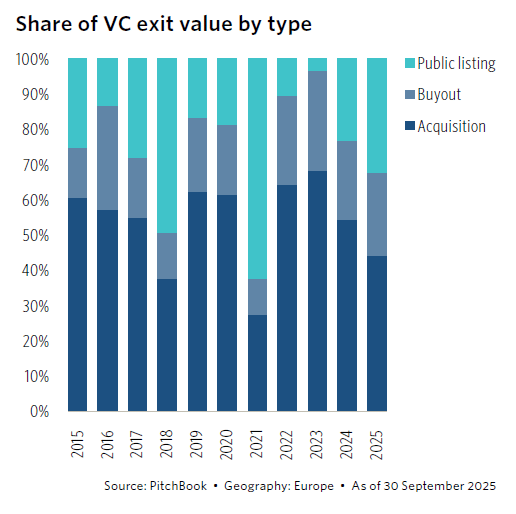

4. Exits rise on the back of Klarna, but the underlying market remains fragile.

Q3 exit value hit €23,8 billion, with Klarna’s long-awaited IPO on NYSE accounting for over half of that total. The €12,7 billion exit was a major milestone for European venture, marking a strong valuation rebound from its 2022 down round. Yet, Klarna’s share price has since slipped 20% below its IPO level, reminding founders and investors that liquidity alone isn’t enough, returns matter.

Strip Klarna out, and the picture shifts: exit value is down 15,3% year-on-year, showing that the broader market is still under pressure. IPOs now make up 32,3% of exit value, but this comes from just 14 listings, confirming that recovery is concentrated in a few big wins. Acquisitions remain the dominant exit route, with over 70% of deals using this strategy. AI continues to lead, with standout M&A deals like Workday’s €940,9 million acquisition of Sana and Cognigy’s €815,1 million round.

5. Fundraising in Europe continues to face headwinds

The Q3 run rate points to a steep 52,3% year-on-year decline in capital raised, driven by smaller fund sizes and a surge in first-time and emerging managers, who now account for a third of all fund closes. Regionally, the UK and Ireland have overtaken DACH with 26,7% of total capital raised, while France and Benelux lag significantly, raising just €0,9 billion. Despite this, €16,4 billion remains open across the top 20 venture funds. If closed by year-end, totals could improve, but LP distributions and venture returns, still under pressure at -1,1% in Q1, will be key to unlocking that capital. With startup investment now outpacing fund capital by 5,2x, the imbalance between deployment and fundraising is becoming harder to ignore.

2025 is not a year of easy wins, but of strategic clarity

As dealmaking slows and fundraising tightens, founders face a market that rewards precision, resilience, and timing. AI continues to dominate, exits hinge on a few outsized events, and venture debt is shifting toward later-stage plays. Liquidity remains a challenge, but capital is still on the table for those who know how to unlock it.

At Dups, that’s exactly where we work. We partner with founders and investors who want to navigate this transition with intention: structuring smarter rounds, exploring alternative financing, and preparing for exits in a liquidity-constrained market. Each year, our investment committee selects 10 high-potential startups for our A–Z Fundraising & Exit Program, managing the full process from strategic preparation to investor introductions and deal execution with our curated network of top-tier funds.

Momentum may be under pressure. But sharper signals mean sharper strategies. Let’s chat!

Let's build your next deal together

Your sparring partner for fundraising, acquisitions, and exits. We bring legal and financial firepower, entrepreneur's speed, and direct access to the right capital.