European VC Q2 2025: momentum under pressure, sharper signals

European VC Q2 2025: momentum under pressure, sharper signals

European VC Q2 2025: momentum under pressure, sharper signals

European venture entered the summer under mixed signals. After a strong Q1, dealmaking slowed noticeably in Q2, reflecting global volatility and investor caution. But beneath the surface, the market is not collapsing : it is compressing. Capital is still flowing, only in more concentrated ways, and the signals emerging from this shift may prove more important than the headline decline.

1. Deal activity slows, but early stage shows resilience

H1 2025 deal value reached €29.2 billion, implying a 5.3% YoY decline if the pace continues. The slowdown came in Q2, when deal value fell 13% compared to Q1. Deal count dropped even faster, underscoring that the problem is less about money and more about volume: fewer investors are putting capital to work. Still, early-stage rounds showed surprising resilience. With €7.8 billion raised in H1, the segment is pacing only slightly below last year. Later-stage rounds continued to dominate overall value, but the fact that early stage held up better than expected suggests that discipline has not yet translated into desertion.

Regionally, momentum is uneven. Southern Europe and Israel both saw activity accelerate, supported by large rounds in Spain, Portugal and Tel Aviv. Meanwhile, France & Benelux contracted by 25.8% YoY, and even the UK & Ireland fell behind last year’s pace. Europe’s venture map is shifting, not just in volume but in geography, with emerging hubs claiming more of the spotlight.

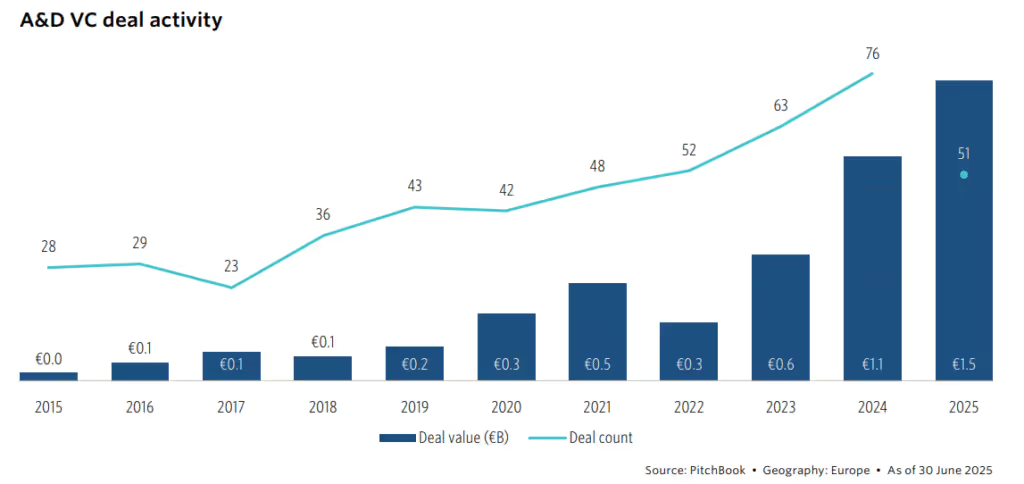

2. Aerospace & defense moves to the core

One of the most striking shifts in Q2 came from aerospace & defence. The sector attracted €1.5 billion in H1, already more than all of 2024. With the EU’s €800 billion ReArm Europe initiative and surging national defence budgets : Germany’s up 23% in real terms last year, defence is becoming a new centre of gravity for European venture.

Companies like Helsing, now having raised over €1 billion, embody this private-public convergence. Central & Eastern Europe is gaining ground in deal count, while DACH still leads in value. Public markets are also reflecting the trend: Rheinmetall and Saab both reported double-digit sales and profit growth in Q1. The message is clear: defence is no longer a niche corner of VC, but a sector reshaped by policy, geopolitics, and capital intensity.

3. AI keeps dominating, but scrutiny is rising

AI continued to capture outsized attention, accounting for 34.5% of deal value in H1, or €10.1 billion. That is remarkable dominance, even if still only half the share AI commands in the US. Some of Europe’s largest rounds this quarter were AI-related: Helsing raised €600 million in Germany, TEKEVER €445 million in Portugal, ATS Holding €407 million in the Netherlands.

But the question is no longer how much capital goes into AI, but into what kind of AI. The PitchBook’s report highlights a distinction between companies with AI at the core of their intellectual property versus those adding AI as a feature to legacy software. Investors are increasingly probing that distinction. Europe risks falling into a pattern where capital flows heavily into AI-labeled companies without always validating the depth of their technology. The signal here is not just dominance, it is the need for sharper due diligence.

4. Venture debt becomes a structural pillar

Venture debt remained strong in H1, with €9.2 billion raised, well below 2024’s record but far above pre-2021 levels. The largest deals in Q2 came from fintech names in the UK: Ferovinum (€478 million), Carmoola (€354 million), Wagestream (€351 million). The median deal size is rising as debt becomes a preferred option for growth-stage companies, which accounted for two-thirds of H1 deal value.

What matters is not the level but the mindset. Founders are no longer using debt only as a bridge, but as a strategic instrument to manage dilution and timing. Debt is now embedded in the European growth playbook, and the question is not whether it will persist, but how it will integrate with equity and secondary capital to create more flexible funding stacks.

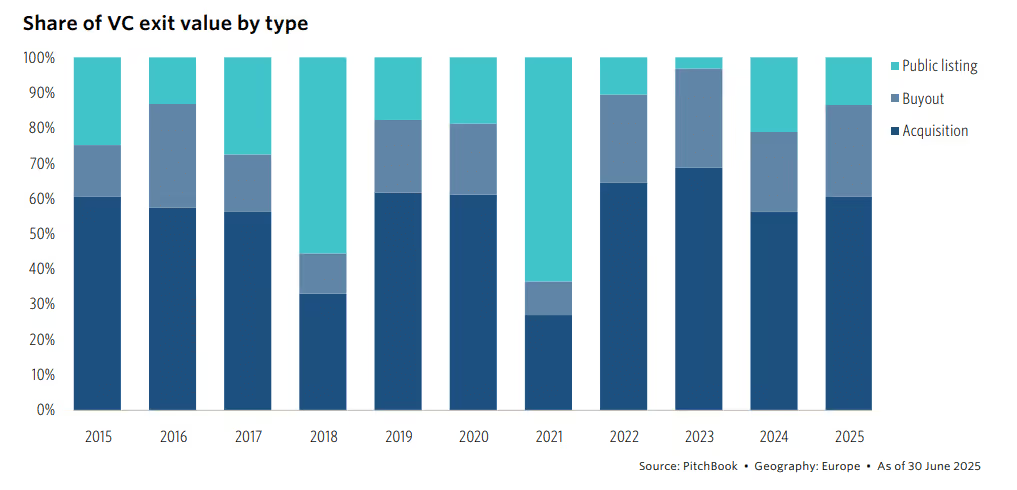

5. Exits lose steam, liquidity remains the bottleneck

After a recovery in 2024, exits slowed again in H1 2025. At €26.8 billion, exit value is pacing 12.3% below last year. Acquisitions remain the dominant path, representing over 70% of volume, with notable deals including EsoBiotec (€942 million) and Brightflag (€425 million). The rare large IPO was eToro’s €3.5 billion listing in Israel.

The real signal is not valuations but liquidity. Even with decent exit values compared to pre-2021 norms, the pace of distributions is not keeping up with the growth of the ecosystem. That creates pressure on LPs and pushes attention toward secondary strategies. In short: the capital cycle is working, but too slowly.

6. Fundraising under heavy pressure

Perhaps the starkest data point of Q2: only €5.2 billion was raised across 65 funds in H1, on track for a 53% YoY decline – potentially a record low. Median fund size fell to €50 million, the smallest since 2019. Emerging managers are capturing a majority of commitments (65.1%), but the overall pie is shrinking.

This disconnect is structural: capital invested in startups is now nearly six times the capital raised by European funds. That imbalance will not be sustainable without stronger liquidity. For the first time, DACH and Israel overtook the UK in fundraising, with Germany leading thanks to large closes by Picus and Bosch VC.

What Q2 tells us is that European venture is compressing but not collapsing.

Capital is still here, but it is flowing differently: fewer deals, larger cheques, sharper scrutiny. AI continues to dominate but must be distinguished between depth and marketing. Debt and defence are no longer side notes; they are structural. And fundraising remains the weakest link, tied directly to liquidity.

The surface looks calm. The foundations are under pressure. And the players who adapt with deliberate, diversified strategies will emerge stronger from this recalibration.

At Dups, that’s exactly where we work. We partner with founders and investors who want to navigate this transition with intention : structuring smarter rounds, exploring alternative financing, and preparing for exits in a liquidity-constrained market. Each year, our investment committee selects 10 high-potential startups for our A–Z Fundraising & Exit Program, managing the full process from strategic preparation to investor introductions and deal execution with our curated network of top-tier funds.

Momentum may be under pressure. But sharper signals mean sharper strategies. Let’s chat!

Let's build your next deal together

Your sparring partner for fundraising, acquisitions, and exits. We bring legal and financial firepower, entrepreneur's speed, and direct access to the right capital.