European VC in 2024: Less noise, more signals

European VC in 2024: Less noise, more signals

European VC in 2024: Less noise, more signals

2024 didn’t feel like a breakthrough year for European venture capital, but maybe that’s exactly why it matters. No record-breaking rounds. No flood of new unicorns. No IPO wave. And yet, beneath the surface, something is shifting. The latest PitchBook report helps us make sense of it: not through flashy headlines, but through the signals hiding in the noise. Here are a few takeaways you won’t read in every summary.

1. The market is learning to live without hype

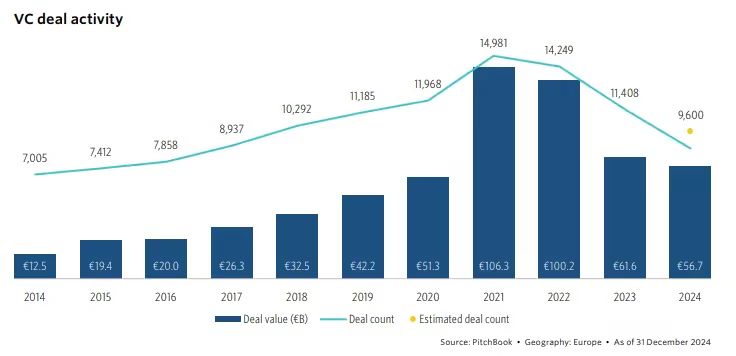

Let’s be honest, 2024 was quieter than most in terms of deal activity. Deal count dropped 23%, deal value shrank 8%. Not exactly festive, but that might not be a bad thing. This quieter period helped filter out short-term bets and hype-driven valuations. The deals that happened this year were more focused, more selective, and often backed by investors who know what they’re doing. Less FOMO, more fundamentals.

In fact, follow-on rounds took the biggest slice of VC money this year. Investors doubled down on their strongest bets instead of chasing new ones. It’s a sign of a more mature market: one that’s becoming more disciplined.

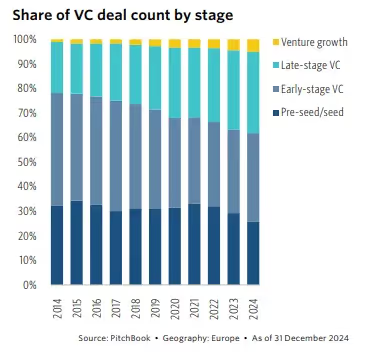

Additionally, one striking trend in the report is how deal value concentrated in larger, later-stage rounds, while smaller, early-stage funding suffered. In some ways, it’s logical: capital is scarce, so it flows where risk is lower. But this “two-speed” VC market could be dangerous. If early-stage teams struggle to raise, tomorrow’s scale-ups won’t exist. And if only the top 5% of companies can access serious capital, the rest of the ecosystem might stagnate.

In terms of geography, the report makes it clear: capital is not really distributed evenly. The UK pulled in over a third of all VC fundraising in 2024. Spain and the Netherlands had a few strong moments, but other regions lagged behind. Emerging funds (younger and smaller VCs) have also been struggling to raise, even though they represent a critical lever for diversity, fresh energy, and new deal flow in the ecosystem. The message is clear: unless we fix how capital is distributed (not just how much is raised), we’ll keep reinforcing the same power dynamics.

2. AI and venture debt are booming but it hides another truth

As expected, AI was everywhere in 2024. The sector pulled in €14.6 billion in VC funding across Europe: nearly a quarter of total deal value. Deal count remained high as well, with over 2,000 AI-related companies active in the region. The UK led the way, hosting the largest AI ecosystem in Europe, followed by France and Germany. But here again, there’s a catch: Europe is still playing catch-up with the US and China in terms of scale, funding depth, and tech infrastructure. In 2023, European startups received just 15% of global AI venture funding, while U.S. companies took more than 50%. That funding gap reflects deeper issues, from talent shortages to slower commercial adoption cycles.

That said, Europe’s strength lies in applied, ethical AI (particularly in sectors like mobility, manufacturing, and healthcare). The UK has become a hub for enterprise software and AI infrastructure, while Germany focuses on industrial automation and France on energy and AI regulation. But fragmented regulation, especially around the EU AI Act, and a lack of late-stage capital still hold many startups back from scaling globally, especially when compared to the more unified U.S. market, where growth capital and go-to-market speed remain unmatched (see our article on the topic).

Besides, venture debt hit record levels in 2024, but behind that figure, there’s something deeper. It’s not just a funding mechanism, it’s a signal: founders are actively looking for alternatives to equity dilution. That tells us something about how cautious they’ve become, and how capital efficiency has become a mindset, not just a metric. It also tells us that the current funding stack might not be serving startups as well as we think. A healthier ecosystem would offer more flexibility, debt, equity, secondary, hybrid: at every stage.

3. Liquidity pressure is shaping behaviour, not valuations

Everyone has been waiting for a valuation correction. But what we are really seeing is a liquidity correction. Many startups aren’t desperate for cash (they still sit on 2021-2022 war chests), but investors are. That’s why secondaries are picking up. That’s why we’re seeing cap table reshuffles and exit prep without the exits. It’s not about what companies are worth, it’s about who needs liquidity first.

This could reshape dynamics in 2025 and beyond. Expect more strategic secondaries, more structured deals, more capital recycling and maybe fewer vanity valuations.

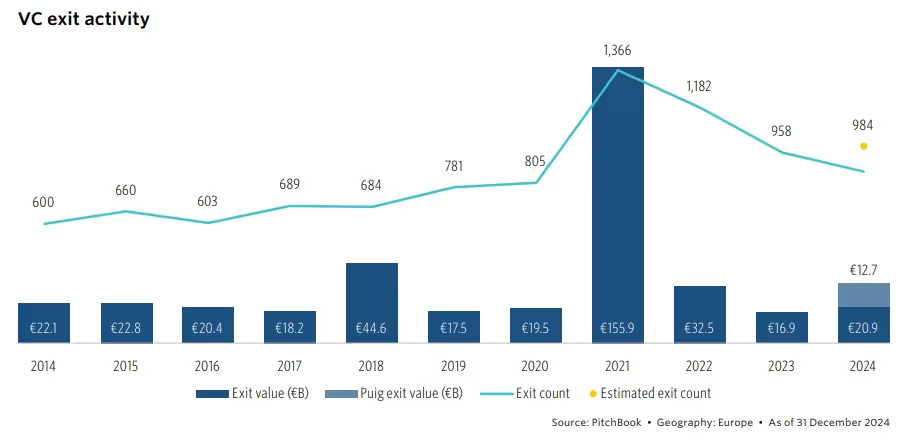

Meanwhile, Exits are starting to come back too (slowly). Indeed, exit value rose by nearly 24% in 2024, but most of it came from a few mega-deals. Public markets (IPO) reopened just slightly, and many founders still hesitate to list. Instead, M&A and reverse mergers took the lead, especially in AI and life sciences.

So, what should we take away from all this?

2024 wasn’t a blockbuster year. But maybe it was a foundational one. A year where:

- Capital got more disciplined,

- Founders got more efficient,

- And the ecosystem started asking deeper questions about how it wants to grow.

At Dups, we see this shift every day. Founders are rethinking their funding paths. Investors are recalibrating their strategies. And everyone’s trying to build smarter, not just faster.

And that’s exactly where we come in as your sparring partner. Whether you’re preparing a fundraising round, exploring funding options, or thinking about a strategic sale, Dups helps you structure the right approach, connect with the right investors, and unlock the right opportunities, at the right time.

Let's build your next deal together

Your sparring partner for fundraising, acquisitions, and exits. We bring legal and financial firepower, entrepreneur's speed, and direct access to the right capital.