European VC Q1 2025: the market is still recalibrating

European VC Q1 2025: the market is still recalibrating

European VC Q1 2025: the market is still recalibrating

In a market that continues to navigate geopolitical tensions, stubborn inflation, and ongoing caution, European venture capital held its ground. Not with fanfare, but with focus.

The latest PitchBook report reveals a market that’s still adapting: pragmatic, irregular, but undeniably alive. Let’s unpack what’s moving beneath the surface!

1. Selective capital, stable hands

The headline number is comforting: €16.7 billion in Q1 deal value. That’s up 10.8% YoY on an annualised basis. But that doesn’t mean money is flowing freely. Deal count continues to decline, and the balance is tilting hard toward later stages. Among the European regions, France & Benelux is pacing the lowest in terms of deal value. Sitting at €2.3 billion in Q1, the run rate implies a 26.3% YoY decline in full-year deal value.

Venture growth deals are pacing to exceed 2024 levels by over 60%. Seed and pre-seed, on the other hand, are shrinking fast. Early-stage teams are still grinding for visibility. The European market is showing signs of maturity but not without cost. A more disciplined capital cycle is good for quality, but risks leaving younger companies behind.

This divergence is increasingly systemic. Capital is not just scarce: it’s choosy.

2. AI keeps climbing, but expectations are sharper

For the first time, AI & ML overtook SaaS in deal value rankings. With €4.6 billion invested, AI now represents over a quarter of all European VC funding. And yet, this isn’t just a capital story: it’s a shift in where conviction lives.

The sector has moved beyond buzzwords. Investors are looking at scalable infrastructure, tangible enterprise use cases, and deeptech crossover with life sciences and industry. The UK remains the epicentre, while France and Germany consolidate their strategic niches.

But let’s be clear: Europe is still catching up in scale and speed. Fragmented regulatory frameworks, including the EU AI Act, continue to drag. And without late-stage depth, many high-potential AI players won’t scale beyond the continent.

3. Debt is rising by design, not desperation

Venture debt cooled after a record 2024, reaching €5.6 billion in Q1. But that slowdown doesn’t necessarily reflect weakness. Nearly half of all venture debt deals now occur at the growth stage. Founders are using it to manage dilution, extend runways, and control timing.

As IPO prospects gradually reopen, many late-stage companies are weighing debt versus equity with greater clarity. This is healthy. A diversified capital stack—debt, equity, secondary is increasingly the new standard, not the exception.

4. Exit markets are cautious, but not closed

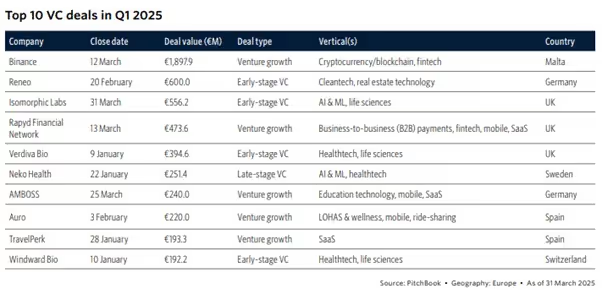

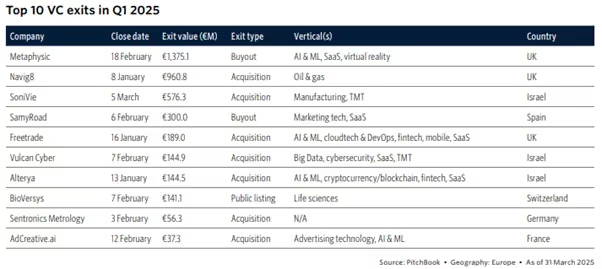

€11.8 billion in Q1 exit value is underwhelming, yes. But the details matter. AI exits are up (€3.7B), with Metaphysic’s €1.4B buyout leading the pack. M&A remains the dominant path. IPOs? Not quite there yet.

Public valuations are holding steady, but political uncertainty (especially from the U.S.) has many founders pressing pause. Klarna, Ebury, I-Care, and others have already delayed their listings. Still, the European pipeline remains rich: over 370 IPO-ready companies are waiting in the wings. If conditions stabilise in the coming months, exits could accelerate fast. But for now, strategic sales will continue to do the heavy lifting.

5. Fundraising is quiet but it’s recalibrating

€2.3 billion raised over 24 funds in Q1 is a modest start. But the structure of that fundraising tells a richer story. Over two-thirds of closed vehicles came from emerging managers. Specialised funds in cleantech, biotech, deeptech continue to attract capital. And regional diversity is improving, with DACH leading, and the UK no longer dominating the charts.

This is less about volume than direction. The European GP landscape is evolving. New voices are coming up. Strategies are sharpening. And LPs, while cautious, are still backing the right stories. However, fundraising is the lumpiest of all the segments of venture activity PitchBook tracks.

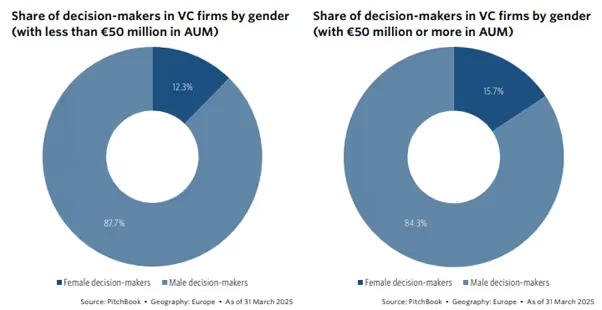

6. Women in VC: slow progress but stronger foundations

In a market searching for efficiency and selectivity, inclusion risks falling off the radar. Yet Q1 data shows that female-founded companies continue to hold their ground. While deal count declined sharply, female founders still raised over €10 billion in 2024, marking a fourth consecutive year at that level. What’s shifting is the nature of those deals: fewer rounds, but larger ones especially at late-stage and venture growth.

But systemic gaps remain. Less than 10% of VC-backed companies in Europe have an all-female CEO team. And while women are slightly more represented in larger VC firms, they still hold under 16% of decision-making roles. Among emerging fund managers, the numbers are slightly better but far from parity.

This isn’t just an equity issue: it’s a pipeline issue. Fewer women writing cheques means fewer diverse deals get funded. And without targeted LP support, the next generation of female GPs may struggle to emerge. If Europe wants a more innovative, resilient VC ecosystem, it needs to stop treating inclusion as a side benefit and start seeing it as a growth driver.

What Q1 tells us is that venture is still adapting

There’s no doubt: this is a more cautious, more uneven environment than we’ve seen in years. But caution isn’t the same as stagnation. And the signals from Q1 suggest something clear: European venture is still recalibrating, as we saw in 2024 (see our article here).

- Capital is consolidating but into stronger hands : Investors are focusing their money on companies with more solid revenues, proven business models, and experienced leadership, rather than spreading it across riskier or earlier-stage bets.

- AI is maturing from hype to infrastructure : Funding is shifting towards AI companies that build essential tools and real-world applications (e.g. healthcare, industry, or enterprise software) instead of speculative or trendy consumer apps.

- Founders are building more carefully, keeping multiple options open: Many founders now structure their growth plans to leave room for different paths (e.g. raising more equity later, using venture debt, selling, or even staying independent longer if needed).

- The funding stack is evolving quietly but structurally: Startups are no longer relying only on equity – they mix venture debt or hybrid financing early on, creating more flexible and resilient funding strategies.

In short: the surface is calm, but the foundations are shifting. And the players who navigate this transition best won’t be the loudest, they’ll be the most intentional.

At Dups, that’s where we focus: the substance, not the splash.

We work with founders and investors who see beyond the quarter, who want to structure smarter rounds, explore financing alternatives, or prepare for exits in uncertain terrain.

Each year, our investment committee selects 10 high-potential startups to join our A-Z Fundraising or Exit Program, where we manage the entire process from strategic preparation to investor introductions and deal execution, with our curated network of top-tier funds.

Quiet momentum is still momentum: let’s build on it!

Let's build your next deal together

Your sparring partner for fundraising, acquisitions, and exits. We bring legal and financial firepower, entrepreneur's speed, and direct access to the right capital.